A crack-up boom

Are Aussie refiners worth a punt?

Capital cycles

The resources sector is fundamentally shaped by long capital cycles. As Rick Rule always says “the cure for high prices is high prices and the cure for low prices is low prices”… which is a short hand way of explaining the phenomenon described in Edward Chancellors book Capital Cycles:

High returns attract capital. More capital leads to more competition, overcapacity and lower returns.

Low returns repel capital. Less capital reduces supply, improves industry economics and leads to higher future returns.

To my mind there is no better (and more topical) part of the resources sector to illustrate the long capital cycles of the resources sector than oil refining.

Refining in the West

Oil refining much like metals refining including aluminium smelting and steel manufacturing have received approximately ZERO Western capital for the past ~50 (!) years.. that may sound like hyperbole and it isn’t exactly accurate to a tee but I challenge you to find when the last greenfield oil refinery, Aluminium smelter, steel mill or metals refinery was built in the West.

In the US - the last greenfield oil refinery - Marathon’s Grayville refinery in Louisiana - was built in 1977 (there have been some expansions done in more recent years).

In Australia - the youngest refinery Lytton is old enough to be a grandfather having been built in 1965. And Australia has infamously got just two operating refineries today after closing 5 facilities in the past ~15years.

In Europe - other than the Leuna refinery built in Germany in 1997 you’d have to go back to 1979/1980 to find the last build.

This is a sector that has been starved of capital for decades after a flood of capital entered the space in the 1960’s & 70’s.

In more recent times refineries have been built in the Middle East (Oman, UAE, Saudi, Kuwait) along with India, China, Malaysia and Nigeria but arguably the new builds have not kept pace with demand after accounting for the constant closures from plants built during the last capital cycle that occurred ~50years ago in the West.

The closest thing to a Western refinery that has been built in the past 20 years is the Olmeca (Dos Bocas) refinery in Mexico. This is a 340kbbl/day project that began construction in 2019 with a budget of US$8bn and a timeline of 3years. And like a typical Western project - the budget blew out from US$8bn to ~US$20bn and the timeline from 3 years to 7 years AND counting having only achieved a processing rate of 260kbbl/day versus the 340kbbl/day design capacity.

The economics of refineries

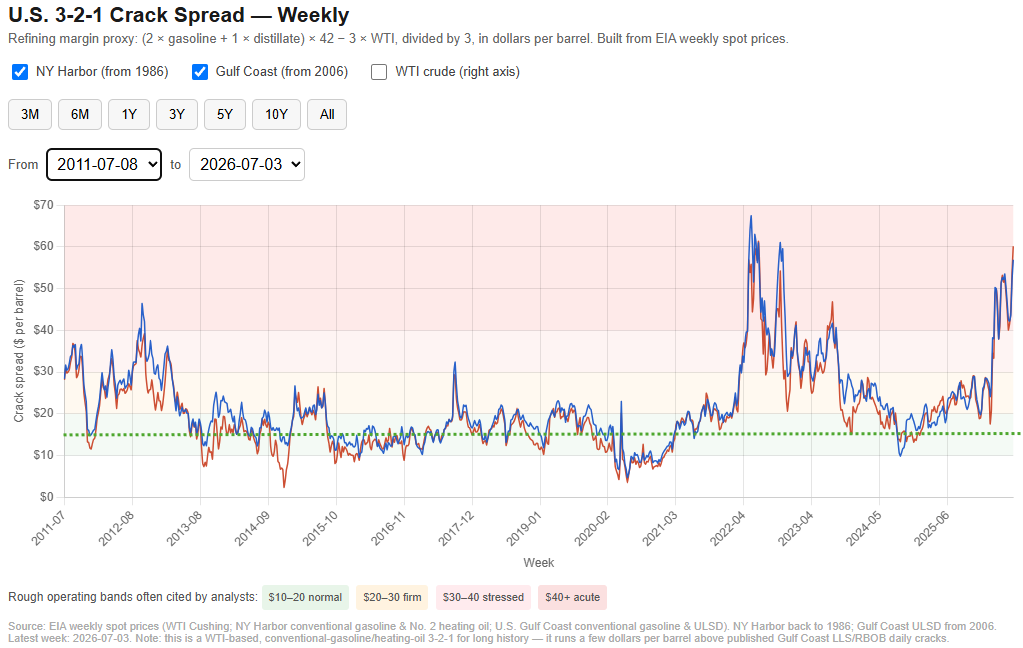

Crack spreads are the spread between the price of crude oil and the price of refined petroleum products (gasoline, diesel, jet fuel et al). They effectively measure the gross margin refineries receive (this is not profit). Below is US 3-2-1 crack spread over the past 15 years and the website where I found this has a cool interactive chart you can cut and dice the time period (access here). The 3-2-1 crack spread is the spread between the cost of 3 barrels of crude oil and the price of 2 barrels of gasoline and 1 barrel of diesel.

Among other things the chart shows that other than a few short blips - crack spreads have been fairly stable at around ~US$15/bbl over the past couple of decades. And again - this spread is not profit as the refiner has a host of costs incurred to convert/‘crack’ crude into refined products.

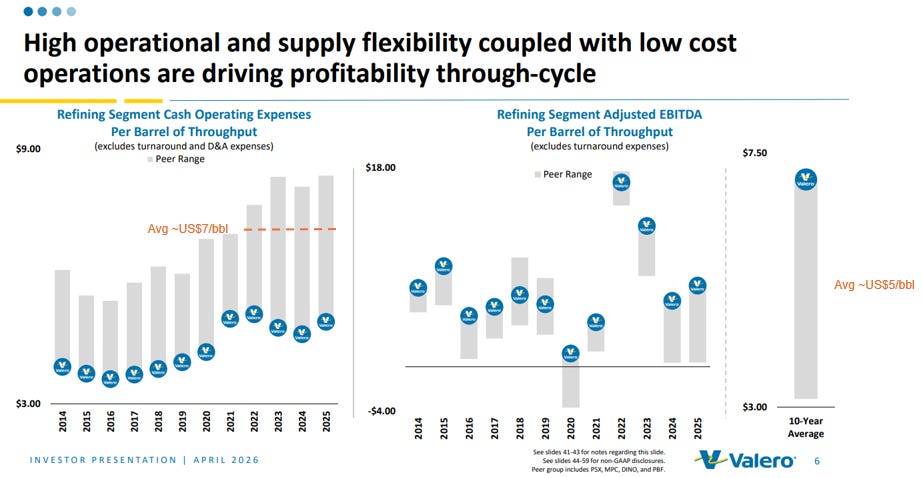

From my look at the operating costs of refiners - the most efficient operate around US$5/bbl opex today and likely the average cost is closer to US$7-8/bbl and you can easily add a further ~US$2-3/bbl in sustaining capital. This chart from US refiner Valero summarises this well.

So whilst crack spreads have averaged ~US$15/bbl over the past couple of decades perhaps the operating profit has been something closer to ~US$5/bbl - an incredibly poor return given the heavy capital outlay to build these things (Olmeca for eg cost ~US$200/bbl initial capex).

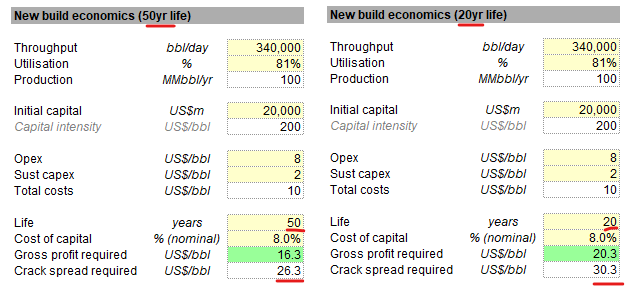

So what are the economics of a new build today? And what crack spread is required to incentivize the construction of a new refinery? My guess using the Olmeca refinery data (recall construction started in 2019 and inflation between then and now likely adds significantly to capital costs) and a basic DCF model we have the below…

I calculate that crack spreads would need to be US$26/bbl for an investor to make an 8% return on investment for a 50 year life refinery. But who in their right mind is committing billions of dollars here in 2026 and taking a bet (to earn a measly 8%) that the world still runs on diesel, gasoline and jet fuel in 50 years time? Even 20 years could be considered a major risk. So my takeaway here is if it were left to the private sector to fund - crack spreads would need to be sustainably above US$30/bbl to attract private capital to invest in new capacity. This is just a data point.

The economics of Aussie refineries

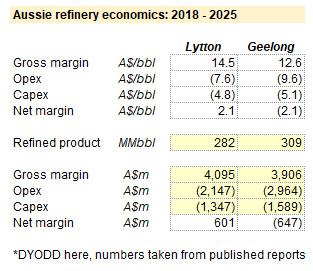

The are just two Aussie oil refineries. The Lytton refinery owned by Ampol (AMD.AX) and Viva Energy’s (VEA.AX) Geelong refinery. Lytton was built in 1965 and has a capacity of 109kbbl/day (~36mmbbl/yr at ~90% utilisation). Geelong was built in 1954 and has a capacity of 120kbbl/day (~40mmbbl/yr at ~90% utilisation). Combined these two refineries supply approximately ~20% of domestic needs with the rest imported via Asian refineries.

To say these have been bad businesses to be involved in over the past decade would be an understatement. Between the two refineries they have basically broken even over an eight year period from 2018 which given the amount of sunk infrastructure being utilised is an incredibly poor investment. And the Aussie refiner economics are reflective of the West and really of the globe.. which brings us back to the message from Capital Cycles - this sector and it’s (lack of) returns has repelled capital.

High returns attract capital. More capital leads to more competition, overcapacity and lower returns.

Low returns repel capital. Less capital reduces supply, improves industry economics and leads to higher future returns.

Today’s Market

Last week crack spreads in Europe hit record highs at ~US$60/bbl - miles above the ~US$15/bbl averaged over the past couple of decades. And whilst I’d like to have said this is a result of the capital cycle and decades of underinvestment (which isn’t exactly untrue) there has been a few other catalysts for this move including:

Russia banning the export of diesel last week following continued attacks on oil refineries from Ukrainian drones.

China banning the export of refined petroleum products from early March following the start of the conflict in the Persian Gulf (this was announced to start being relaxed last week).

Damage to numerous refineries in the Middle East from the conflict between Iran and US/Israel.

Various other failures and maintenance shutdowns to other refinery’s (which is what happens when they get to old age and are starved of capital).

Crack spreads have even materially diverged from crude oil - which has collapsed in the past few weeks following a supposed cease fire… whether this is a temporary phenomenon or not is up for debate but it should be noted that there is no strategic diesel, gasoline or jet fuel reserve like there is crude oil - so the buffers that exist in the crude market do not exist in refined products.

As I said in my prior note - I try to stick to my lane when it comes to speculating - which is certainly not the oil market and is most certainly not geopolitical events… but you cannot avoid geopolitical events as a resource speculator - just look at some of the prior opportunities we took advantage of such as First Quantum’s woes in Panama or Trilogy’s joys in Alaska. All we can do is assess what’s priced in to various investment opportunities and whether they represent a favourably skewed risk/return speculation.

Investment Opportunities

We’ve established a few things thus far:

Crack spreads are at record prices;

There has been a chronic underinvestment in refining capacity in the West for at least the past three decades;

New builds today require crack spreads sustainably above US$30/bbl to generate a sufficient return for private capital in the West to invest in new capacity (well above the ~US$15/bbl in recent years).

The other point I want to make is the geopolitical events that have helped to cause a crack up boom in crack spreads have also shined a light on the vulnerability of Western supply chains so much so that existing Western refinery’s are now being classed as critical infrastructure by government.

This last point is quite important as government policy has shifted from being neutral/unsupportive of the sector to being a major supporter. This is no more evident than in Australia where in response to the conflict in the Middle East the government announced, among other things, changes to the Fuel Security Services Payment (FSSP) on the 20th of March. This payment effectively ‘tops up’ the crack spread paid to refiners to ~A$16/bbl (10c/L) if it falls below this level up to a maximum of ~A$3/bbl (1.8c/L).

All of the above is an excellent backdrop IMO to potentially turn what have been horrible investments in refinery’s that have returned next to nothing in the past decade to perhaps something that is far more profitable in both the short and medium/longer term.

Whilst there are a few ways to speculate on crack spreads and oil refineries I want to focus on the two opportunities on the ASX to begin with (mentioned above). But here is a handy list of names below in the US which, as a basket, are breaking out to new all time highs and may be worth a look in the future (especially given they are closer to pure play refiners than the Aussie names I’m about to look at).

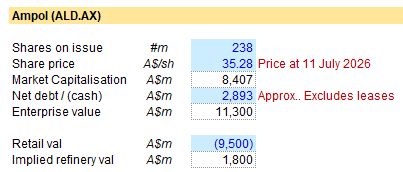

AMPOL (ALD.AX)

Retail arm

As mentioned above the difficulty in playing the Aussie refiners is the oil refining part is (or has been) a small part of the overall business with both Ampol and Viva operating a huge network of retail service (aka petrol/gas) stations across the country. These convenience stores sell all manner of retail products (typically food and beverage) in additional to gasoline/petrol.

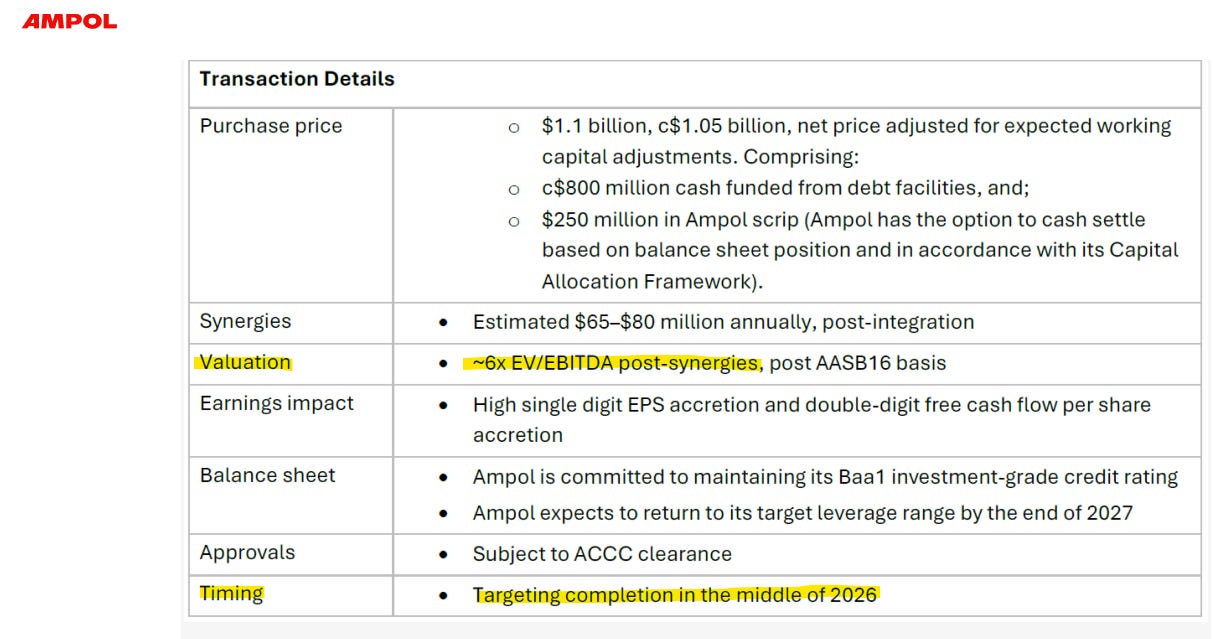

Ampol has the largest network of service stations in Australia. Following the recent acquisition of EG Australia (approved by Australia’s competition authority ACCC in recent weeks) Ampol now has around ~1,100 stores in Australia and a further ~500 stores in New Zealand.

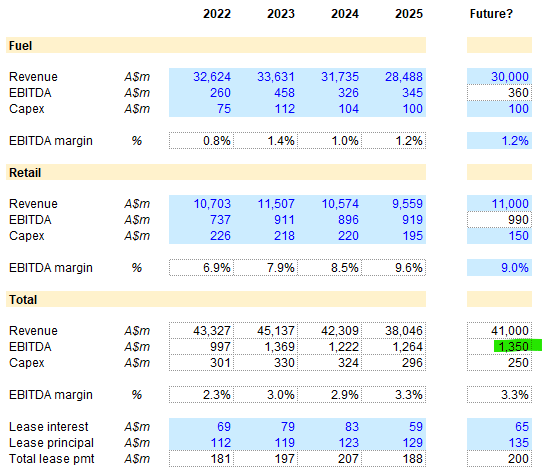

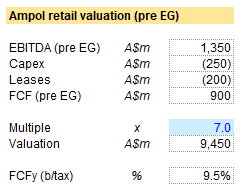

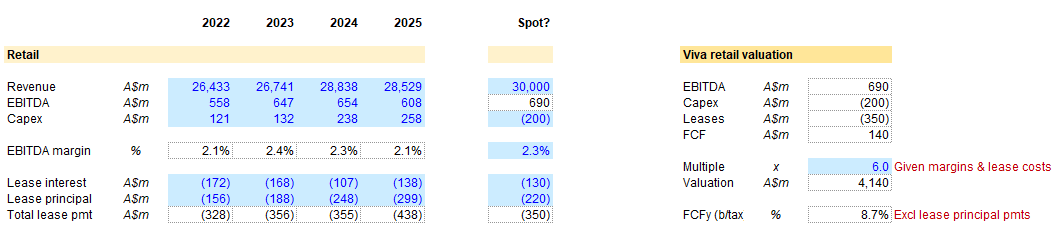

I don’t wish to go into much detail on the retail arm of the business as the focus is on the oil refining component.. but we do need to come up with a ballpark valuation of this component of the business. So what I’m going to do is real simple which is value the Ampol retail business at 7x EBITDA which is slightly higher than what Ampol paid for EG (done at 6x EBITDA) but reflects a higher quality / higher margin business.

A couple of things to note though:

these service stations are typically leased (from what I can see Ampol and Viva either sold or spun out the properties the service stations stand on into a REIT last decade)… the lease costs are not in EBITDA - so we will look at this separately.

the illegal cigarette market that has popped up has taken away a not insignificant high margin sale item from these service stations (we will just note this for now).

Looking at historical revenues and margins for this part of the business and making an assessment on whether these trends hold - I have created the above. And this quite simply lands us at a valuation below of ~A$9.5bn for the retail arm of the business pre the EG acquisition which was done at A$1.1bn (I have not accounted for either the cash outflow or the earnings/value of this business in my valuation).

And looking at the above… a 7x EBITDA multiple lands around 9.5% FCF yield (pre-tax, maybe 7% post tax) which seems fair.

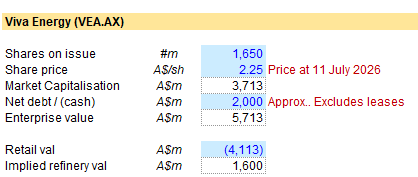

If we back out the value of the retail arm from Ampol’s valuation today I estimate the implied value of the Lytton refinery is approximately A$1.8bn. If we assume the 36mmbbl/year output mentioned above this places the refinery at a valuation of A$50/bbl of annualised production. This is a very handy data point.

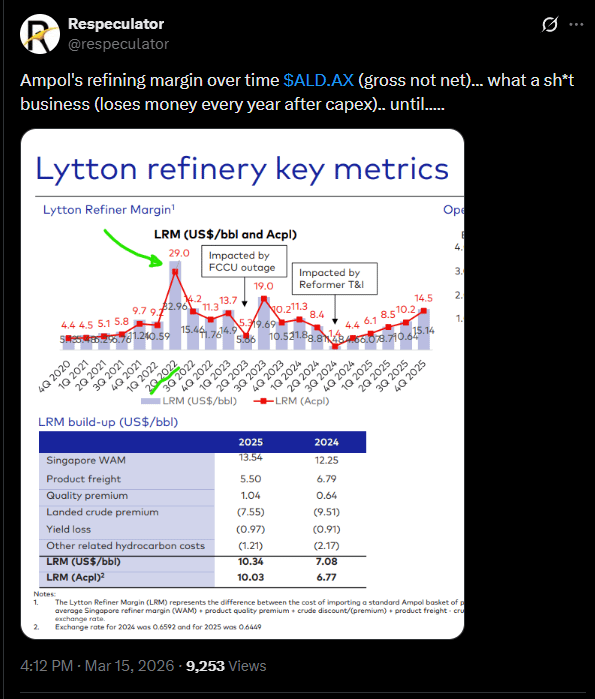

Lytton refinery

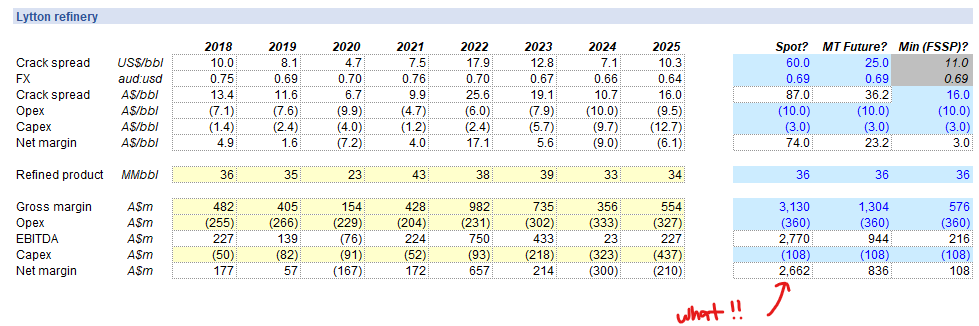

As mentioned above the Lytton refinery has capacity of ~109kbbl/day or around ~36mmbbl/yr at a ~90% utilisation. Its costs have been around ~A$15/bbl the past couple of years (~A$10/bbl opex + ~A$5/bbl sustaining capex). There has been A$1bn of capital spent at the refinery in the past 3 years - a large chunk of this has been executing the Ultra Low Sulfur Project which is to bring the refinery in compliance with new government standards where sulfur levels in gasoline must be below 10ppm. Another chunk has been catch up capital maintenance.

The data above speaks for itself. At spot prices the refinery is potentially making ~A$2.7bn per annum (!!). Remember we calculated an implied value of the refinery above as A$1.8bn.. so you really don’t need much time at current crack spreads to achieve our market valuation… ~8 months will do it. And this just highlights the torque the refinery valuation has to crack spreads.

So valuation is really a thumb suck given how torqued margins are to crack spreads and how unpredictable crack spreads are. For me I am thinking about it this way….

Accounting for the past quarter of earnings where cracks were ~US$30/bbl. At this price point I think Lytton could have made something like A$350m for the quarter (pre-tax);

Making an assumption on how long spot crack spreads stay this elevated: For the base valuation I am assuming a quarter of US$45/bbl average cracks (spot is ~US$60/bbl). For the upside case I am assuming cracks average out at US$45/bbl for the next six months whilst for the downside I’m assuming cracks average US$25/bbl in Q3 before settling back. (*Note that Lytton is scheduled to go down for maintenance in August - I will just note this for now and not account for);

Making an assumption on medium/long term crack spreads. For the base valuation I am assuming crack spreads have left the prior ~US$15/bbl price regime and will sit closer to new build incentive prices at US$25/bbl. This is the same for the upside case. For the downside case I am assuming they head back down to the US$15/bbl price regime;

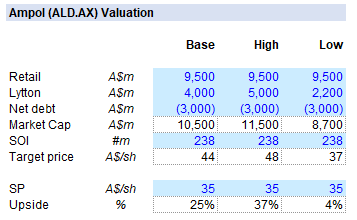

Apply an appropriate multiple - I’m going to use 3.0x for the base and low cases and 3.5 for the upside. This may seem conservative given the potential remaining life of the refinery - but I don’t want to be punting on a large multiple here and there is zero terminal value in these refineries (just a big clean up bill).

This is where it lands us:

Approximately A$4bn (US$2.8bn) or US$75/bbl in the base case which is far below that of replacement cost today (Olmeca: US$200/bbl). And the best thing here in my view is even the low case doesn’t seem to be priced in.. so the market is assuming cracks basically hit the floor (~US$15/bbl) in the next few weeks and stay there.

VIVA

I’m conscious this is getting lengthy so I’m just going to provide data only for Viva below. The only thing to note here is this refinery caught fire in April - and there is a potential repair bill (and/or insurance claim) and timeline to get operations back to capacity. The company has disclosed they are back to 90% capacity in late June.

Retail - valuation ~A$4bn using a similar methodology to Ampol (lower multiple at 6x given lower margins and quality of business plus more costs shifted into lease payments).

This gives us an implied valuation of the Geelong refinery at A$1.6bn.

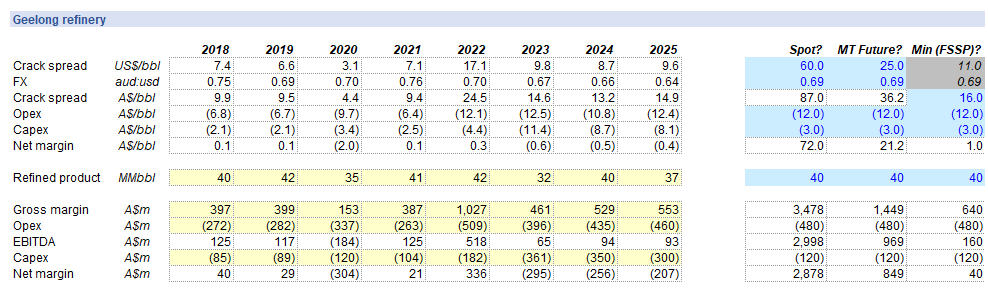

The refinery data is similar to Lytton - slightly higher unit operating costs and more production. They too have the elevated capex in the past few years to bring the refinery up to new compliance standards regarding sulfur levels.

Below is the refinery valuations based on the same cases as Ampol. Note I have adjusted Q2 lower just based on the refinery being down for a few weeks in April and May due to the fire.

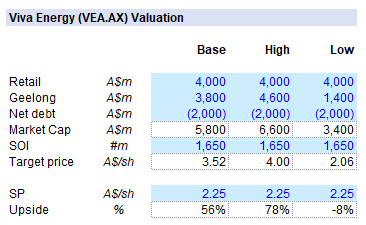

The valuation shows a similar story - a highly levered play on crack spreads, even with the retail arm taking up the bulk of the valuation. Viva is even more levered given its relative debt levels and higher cost / lower margin business.

Summary

Refining oil has been a poor returning business for the past couple of decades and the low returns have repelled capital - especially in the West.

Now - following some geopolitical conflicts that have caused damage to numerous refineries across the globe crack spreads have become sexy again - hitting all time highs last week in the wake of news that Russia will ban diesel exports.

In the West oil refineries are now critical infrastructure - and Governments like that in Australia have stepped in to subsidise returns… just like they have done for coal fired power (see Eraring), steel (see Whyalla) and Aluminium (see Tomago).

The two refineries in Australia - Lytton and Geelong - are incredibly torqued to crack spreads. The question we need to ask is whether the current elevated crack spreads - especially relative to the crude oil price - is a temporary phenomenon… and to what degree.

It appears on my elementary math that the market is pricing in crack spreads to fall through the floor in the coming weeks and trend back down to the ~US$15/bbl price regime it has been in for the past couple of decades and where refiners have made little to no margin. That to me makes for a decent risk/reward set up as you are paying arguably little to no premium despite cracks being at all time highs.

I’m taking a small bet here on the Aussie refiners - especially after the recent pullbacks… I have no view on the geopolitical situation/s happening but the risk/return seems okay at current market prices. This is in no way a recommendation… please seek your own personal advice.

Best

Respeculator

PS - as I mentioned last note… I would love any pushback on the above and any further intel from those closer to the oil refining business. I am just rambling and shooting from the hip.

Last year there was some news “The Australian government said on Wednesday it would invest A$1.1 billion ($735 million) in the development of a low-carbon fuels industry”.

Do tou know more about,this? Are the current refineries getting any part of that for modernization etc? Or is that for completely new competition that would also, in a sense, screw up the capital cycle?

https://www.reuters.com/sustainability/climate-energy/australia-promises-735-million-launch-biofuel-industry-2025-09-17/

A good read regarding the refining sector, in particular US refiners https://hfirideas.substack.com/p/public-us-refiners-strong-fundamentals?utm_source=share&utm_medium=android&r=cvi86